Hong Kong Employer's Return: Filing IRD Forms BIR56A & IR56B Guide

BIR56A Form: What It Is and Who Must File It

Hong Kong employers are legally required to report employee earnings to the Inland Revenue Department (IRD). Failure to do so accurately can result in penalties. The BIR56A form is one of the core documents in this process.

Definition and Purpose

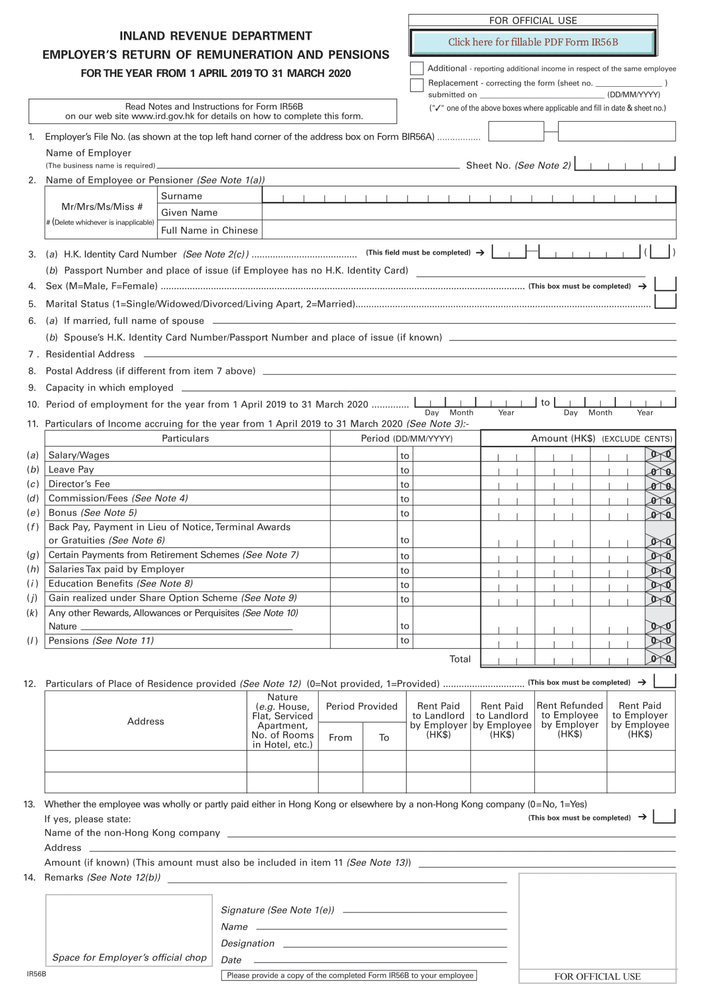

The IR56A is an employer's return form used to report employee income to the IRD for tax assessment. It summarises employment details for a given tax year and acts as a cover sheet, submitted together with IR56B forms which contain individual salary details for each employee.

Who Must File Form BIR56A

Any company or business that employs staff in Hong Kong must complete the IR56A, regardless of size or sector. This covers:

- Private companies with full-time or part-time staff

- Public organisations and statutory bodies

- Non-profit associations with salaried employees

- Overseas companies with staff based in Hong Kong

Freelancers and independent contractors are generally not covered unless they qualify as employees under Inland Revenue rules.

What Triggers the Filing Obligation

Employers must file a BIR56A annually, typically at the beginning of April. Separate forms may also be required when:

- An employee leaves the company

- An employee plans to leave Hong Kong

- A new employee joins during the year

These situations may involve filing additional forms such as IR56F or IR56G.

Key Deadlines for Submitting BIR56A

Annual Submission Deadline

The IRD issues the Employer's Return the BIR56A around early April each year. Upon receipt, employers must submit the following within one month:

- The IR56A form (cover page)

- All related IR56B forms for each employee

If the BIR56A has not arrived by mid-April, employers are still responsible for notifying the IRD. The deadline remains the same regardless.

Deadlines Triggered by Employment Changes

Specific employment events carry their own filing deadlines:

Employee leaves the company — Submit the IR56F form no later than one month before the termination date.

Employee plans to leave Hong Kong — Submit the IR56G form at least one month before the departure date. All final payments must be withheld until the IRD grants clearance.

New employee joins during the year — No immediate filing is required, but the individual's income must be included in the annual IR56B submission.

Extensions and Late Submissions

The IRD may grant an extension if requested in writing before the due date. Late filings can result in penalties, audits, or a loss of compliance status.

How to Complete the IR56A Form

Step 1: Download the Form

Download the latest version of the IR56A directly from the IRD's official website. Do not use older versions, as these may no longer be accepted.

Step 2: Enter Employer Details

The top section requires company information, including:

- Employer's file number (as shown on the BIR56A)

- Business registration number

- Company name, address, and telephone number

- Nature of business (e.g., trading, consulting, services)

Cross-check these details against your business registration certificate before proceeding.

Step 3: Confirm the Tax Year and Sign

Enter the relevant assessment year (for example, 2023/24) and tick the box confirming which IR56 forms are enclosed, usually IR56B. Then complete:

- Full name of the signing officer

- Their position (e.g., Director or HR Manager)

- Date of signing

Only someone authorised to act on behalf of the company should sign the form.

Step 4: Prepare the IR56B Forms

Each IR56A must be accompanied by a completed IR56B form for every employee. The number of IR56B forms must match the total entered on the IR56A cover sheet.

Typical fields on each IR56B include:

- Employee's full name and HKID number

- Position held and employment period

- Total income paid during the year

- Allowances, bonuses, and housing benefits

Step 5: Submit to the IRD

Forms can be submitted in two ways:

- By paper — Post to the IRD's address with all forms enclosed.

- Electronically — Use the e-Filing service via eTAX or the IRD's ER e-Filing software.

Electronic filing is generally faster and provides immediate confirmation of receipt.

What Information Must Be Included in the IR56A

Employer Identification

The form requires the following business details:

- Employer's file number (found on the Employer's Return, BIR56A)

- Business registration number (8-digit identifier from the Hong Kong Companies Registry)

- Registered company name

- Postal address and contact telephone number

- Nature of business (e.g., education, trading, logistics)

Employment Summary

This section gives the IRD a picture of your staffing situation during the relevant tax year:

- Total number of employees for whom IR56B forms are submitted

- Whether any employees joined or left during the year

- Confirmation of any employees who departed Hong Kong

Where staff left mid-year or relocated overseas, the corresponding IR56F or IR56G forms must also be submitted.

Declaration and Signature

A responsible officer must sign the declaration at the bottom of the form, confirming that all information provided is accurate and complete. The form requires:

- Full name of the signing officer

- Position within the organisation (e.g., Director, Manager)

- Signature and date

IR56A in Termination, Resignation, and Departure Cases

The annual IR56A is not the only filing obligation employers carry. When a staff member leaves the company or Hong Kong, additional forms apply and missing the deadlines can lead to penalties or complications with the employee's tax clearance.

Resignation or Termination

When employment ends whether through resignation, termination, or contract expiry employers must file an IR56F form to notify the IRD.

Deadline: The IR56F must be submitted no later than one month before the termination date.

Required details include the last day of employment, reason for leaving, final payment figures, and any unused leave paid out. This applies even where the departure is amicable and the employee remains in Hong Kong.

Employee Leaving Hong Kong

If an employee is departing Hong Kong permanently or for an extended period, the employer must file an IR56G.

Deadline: Submit at least one month before the departure date.

All final payments including salary, bonus, and leave encashment must be withheld until the employee obtains a Letter of Release from the IRD. This process confirms that outstanding taxes have been settled before the individual leaves.

Directors and Consultants

Filing obligations also apply to directors or consultants who continue receiving income after stepping back from active duties. Any arrangement of this kind must be formally closed through an IR56F or IR56G, depending on the individual's plans.

The IR56A Still Applies

The IR56F and IR56G handle specific departure events, but the IR56A must still be filed as part of the annual Employer's Return. It must account for all employees current and former who were on the payroll at any point during the assessment year.